The landmark announcement that there are 300 firms competing for 50 oil blocks in Nigeria’s ongoing upstream licensing round represents a monumental paradigm shift in global energy capital allocation. Historically, sourcing premium upstream production fields was an exclusive playground reserved for a small circle of international oil majors. Today, the current bidding cycle presents a radically altered environment. It is heavily defined by aggressive indigenous corporate participation, automated regulatory portal verifications, and systemic fiscal restructurings under the watchful eye of the Nigerian Upstream Petroleum Regulatory Commission (NUPRC).

For institutional financiers, sovereign energy funds, and global resource analysts mapping out long-term West African energy trends, observing 300 firms competing for 50 oil blocks indicates a massive restoration of macro-market confidence. This extraordinary rush follows years of frustrating regulatory bottlenecks that stalled foreign direct investment before legislative restructuring. As technical evaluations conclude and commercial phases transition ahead of the next major licensing roadmap, understanding the financial and structural forces powering this historic bidding war is crucial for calculating future risk-adjusted yields.

Why 300 Firms Competing for 50 Oil Blocks Matters to Global Investors

The presence of 300 firms competing for 50 oil blocks matters immensely to international asset managers because it serves as a reliable case study on how regulatory clarity can trigger immediate capital migration. When governments provide transparent, non-discriminatory frameworks, risk premiums drop across the board.

Globally, energy groups are actively hunting for low-cost, high-volume production terrains. Nigeria’s massive proved reserves provide exactly that baseline, provided the operational rules remain stable. The intense volume of qualified applications proves that the global energy sector does not lack deployable capital; rather, it seeks jurisdictions where institutional rights are protected and investment cycles are predictable.

Additionally, this competitive environment directly changes the pricing dynamics of signature bonuses and production-sharing contracts. With hundreds of bidders moving through the pipeline, the market itself creates highly transparent asset pricing, ensuring that only technically competent and financially stable entities secure exploration rights.

The Competitive Landscape Behind 300 Firms Competing for 50 Oil Blocks

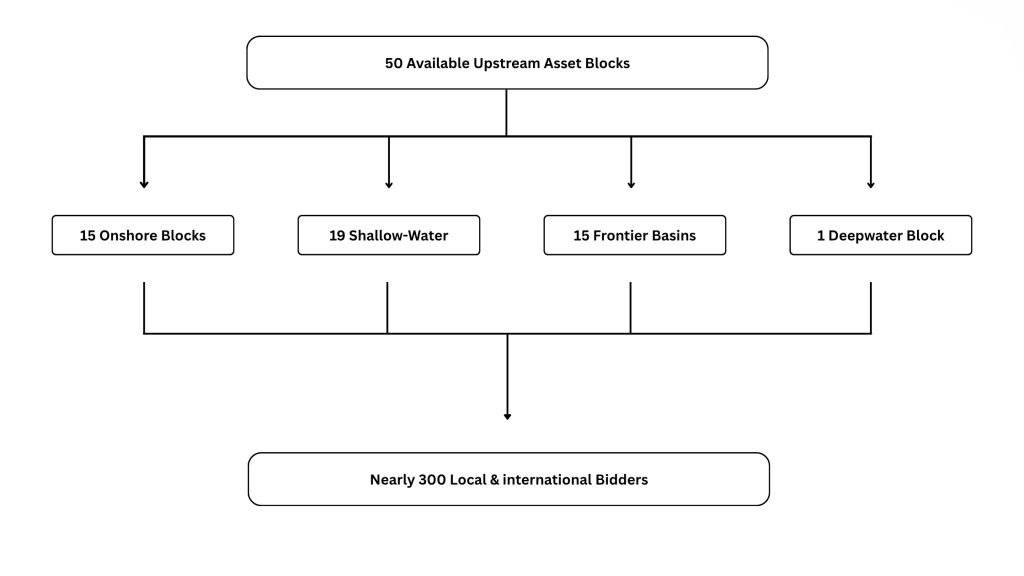

The severe supply-demand gap within this licensing round has completely reshaped sub-Saharan exploration strategies. The NUPRC formally revealed that the blocks span highly diverse geological terrains, ensuring that companies can bid on assets that match their specific engineering skill sets and financial risk profiles.

The 50 available blocks are distributed across four distinct operational terrains:

- 15 Onshore Blocks: These fields feature well-documented geology and require lower initial capital, making them prime targets for local independent operators looking for fast commercialization timelines.

- 19 Shallow-Water/Swamp Blocks: Prolific and heavily mapped, these assets offer relatively straightforward paths to production, attracting mid-tier international consortia.

- 15 Frontier Basin Blocks: Located in underexplored inland plays, these blocks offer progressive tax incentives designed to attract long-term exploration groups looking to expand national reserves.

- 1 Deepwater Asset Block: A high-impact, capital-intensive play engineered for global supermajors with the advanced deep-water technology needed to extract deep offshore reserves.

Because 300 firms are competing for 50 oil blocks, the NUPRC discarded slow, opaque manual processing methods. Bidders must now interface with an end-to-end digital portal that verifies technical competencies, beneficial ownership identities, and financial histories in real time, creating an open and fair bidding environment.

How the Petroleum Industry Act Encouraged 300 Firms Competing for 50 Oil Blocks

The underlying force driving this surge of interest is the structural foundation laid down by the Petroleum Industry Act (PIA). For decades, ambiguous fiscal regimes and complex regulatory frameworks made long-term capital deployment highly risky. The PIA successfully resolved these issues by establishing a modernized dual-regulatory system, introducing progressive royalty structures, and streamlining dispute resolution processes.

PIA Legislative Framework ──► Enhanced Fiscal Incentives ──► Surge in Investor Applications ──► 300 Bidders Engaged

To fully capture value within this updated legal landscape, arriving operators must align their corporate models with sophisticated compliance systems. Leveraging professional Tax Management Services in Nigeria is vital for navigating the progressive hydrocarbon tax changes, production allowances, and environmental remediation fees required under the PIA. Companies that structure their tax profiles early can better handle initial capital expenditures and improve long-term dividend payouts.

Indigenous Operators Driving the 300 Firms Competing for 50 Oil Blocks Trend

The fact that there are 300 firms competing for 50 oil blocks highlights a major trend: the rapid growth of independent African exploration firms. As international oil majors optimize their global portfolios and transition toward deepwater operations, agile domestic firms are actively acquiring onshore and shallow-water assets.

| Operational Terrain | Total Blocks | Primary Target Profile | Capital & Local Content Dynamics |

| Shallow-Water / Swamp | 19 Blocks | Local Independent Alliances & Mid-Tiers | Medium Capital / High Local Content Requirements |

| Onshore Basins | 15 Blocks | Native E&P Firms & Exploration Startups | Low Capital Entry / Faster Time-to-Market |

| Frontier Terrains | 15 Blocks | Diversified Conglomerates & Strategic Bidders | High Exploration Focus / Tax Holiday Benefits |

| Deepwater Fields | 1 Block | Global Supermajors & Sovereign Funds | Billion-Dollar Commitments Needed |

As indigenous firms secure a larger operational footprint, their management teams must run lean, highly professional corporate structures. Understanding The Benefits of Outsourcing Business Operations allows growing exploration brands to delegate non-core tasks like human resource management, international payroll, and administrative compliance to specialized partners. This operational agility frees up executive teams to focus completely on what matters most: geology, extraction efficiency, and pipeline security.

Compliance Challenges

While securing an asset is a major victory, executing a successful exploration campaign requires meeting strict regulatory guidelines. The NUPRC enforces rigid standards regarding host community development trusts, strict zero-flare policies, and carbon reduction milestones. This means bidders cannot simply rely on financial strength; they must demonstrate comprehensive environmental, social, and governance (ESG) blueprints.

Logistics pose another major challenge, particularly for offshore and shallow-water assets. Integrating exploration activities with dependable Offshore Support Services in Nigeria ensures that marine crew transport, heavy-lift supply logistics, vessel leasing, and safety compliance run smoothly. Partnering with proven marine support networks protects operators from costly project delays, allowing them to accelerate production once the NUPRC formally issues their licenses.

Financial Modeling Strategies

To ensure corporate treasuries avoid overextending during this highly competitive cycle, reservoir engineers and private equity investors use advanced quantitative analysis. When there are 300 firms competing for 50 oil blocks, calculating a precise risk-adjusted Net Present Value (NPVasset) protects institutional capital from bid inflation.

The asset value can be calculated using the following display equation:

Where:

- Qt = Expected annual crude oil or natural gas production volume in year $t$.

- Pt = Projected market price of global benchmark crude (e.g., Brent) adjusted for local API gravity differentials.

- Φroyalty = The progressive royalty rate mandated by the NUPRC, varying by terrain depth and daily output volume.

- Ψtax = The applicable corporate tax and hydrocarbon tax rate under current PIA provisions.

- CAPEXt / OPEXt = Capital and operational expenditures, including initial data leasing, drilling infrastructure, and ongoing maintenance.

- Λlocal_content = Required capital investments for local human capital development, community trust funds, and environmental remediation.

- r = The institutional discount rate factoring in country risk and weighted average cost of capital (WACC).

- ∑Nt=1 = The risk-premium multiplier reflecting bid inflation caused by having 300 companies competing for 50 oil blocks.

What 300 Firms Competing for 50 Oil Blocks Means for Nigeria’s Energy Future

The macro effects of having 300 firms competing for 50 oil blocks align perfectly with Nigeria’s domestic refining expansion. According to reports from the Petroleum Technology Association of Nigeria (PETAN), the country’s local refining capacity is growing rapidly, driven by the scaling up of the Dangote Petroleum Refinery and the modernization of state-owned refineries. This means newly awarded blocks will have access to an immediate, high-volume domestic market, reducing exposure to volatile international shipping routes.

Upstream Extraction ──► Direct Crude Supply Pipeline ──► Domestic Refineries ──► Regional Product Distribution

To manage these integrated asset pipelines efficiently, forward-thinking operators are restructuring their workforces. Monitoring emerging Remote Work Trends in Africa allows energy groups to build hybrid teams where geological data analytics, reservoir modeling, and accounting are handled via secure cloud platforms. This approach significantly lowers office overhead, keeping capital focused directly on field extraction.

Ultimately, the competitive drive shown by these 300 firms competing for 50 oil blocks confirms that West Africa remains a vital pillar of the global energy mix. By matching deep technical capabilities with modern compliance models, successful bidders can protect their investments and unlock lucrative, sustainable production across the region.

{kind=link}

{kind=link}